In October 2021, more than 130 countries – representing more than 90% of global GDP – agreed to implement a minimum tax regime for multinationals, ‘Pillar Two’. In December 2021, the Organisation for Economic Co-operation and Development (‘OECD’) released the Pillar Two model rules (the Global Anti-Base Erosion Proposal, or ‘GloBE’) to reform international corporate taxation. Large multinational enterprises within the scope of the rules are required to calculate their GloBE effective tax rate for each jurisdiction where they operate. They will be liable to pay a top-up tax for the difference between their GloBE effective tax rate for each jurisdiction and the 15% minimum rate. If the GloBE effective tax rate domestically is 15% or more, no GloBE top-up tax will be payable. It is the ultimate parent entity of the multinational enterprise that is primarily liable for the GloBE top-up tax in its jurisdiction’s territory.

The goal is to end the ‘race to the bottom’ on tax rates worldwide, under which countries had been competitively cutting corporate taxes to attract businesses, with the impact that other countries felt forced to cut taxes to compete.

The GloBE rules include two main components: the Income Inclusion Rule (‘IIR’); and the Undertaxed Payment Rule (‘UTPR’). Top-up tax is first imposed under the IIR on a parent entity with an ownership interest in a low-taxed subsidiary. The UTPR is a backstop mechanism if there is low-taxed income from an entity within the group that is not brought into charge under the IIR by applying a top-up tax in the jurisdiction that introduced the UTPR.

Top-up taxes calculated under the IIR are to be paid in the jurisdiction of the parent entity of the multinational group, rather than in the low-tax territory that triggers the excess payment. Top-up taxes calculated under the UTPR are to be paid by the entity that operates in a jurisdiction that has enacted the UTPR, even if this entity is not a parent entity of the group. Thus, the Pillar Two rules provide for the possibility that jurisdictions might engage in domestic tax policy reforms and introduce their own qualified domestic minimum top-up tax (‘QDMTT’) based on the GloBE mechanics to avoid any ‘tax leakage’ in anticipation of the GloBE rules becoming effective.

Notwithstanding any new local minimum tax regime which might be designed to reduce or eliminate the GloBE top-up tax, additional top-up tax under GloBE might still be due. This will depend on the local effective tax rate calculation according to the specific rules set out in the Pillar Two regulations.

Definitions of terms used in this publication GloBE effective tax rate = GloBE tax expense/income ÷ GloBE profit/loss Statutory tax rate = Enacted tax rate IAS 12 effective tax rate = IAS 12 tax expense/income ÷ IFRS profit/lossThe Pillar Two rules apply to multinational enterprises that have consolidated revenues (which, as defined by the OECD, include any form of income and are therefore not limited to revenue recognised in accordance with IFRS 15) of €750m in at least two of the last four years.

Pillar Two applies if a jurisdiction in which the group operates has passed the rules into national legislation – this could be the jurisdiction of the ultimate parent entity or, if the IIR Pillar Two legislation is not yet in effect in the ultimate parent entity’s jurisdiction, an intermediate parent entity in the multinational enterprise that is subject to top-up tax. For UTPR, this could even just be a subsidiary in the multinational enterprise. Enacted QDMTT rules could also increase the tax liability of the group.

A multinational enterprise might therefore be subject to Pillar Two taxes, and within the scope of the IAS 12 disclosure requirements, even if the jurisdiction of the ultimate parent entity has not yet enacted the Pillar Two rules.

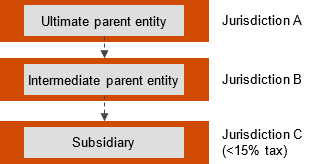

Illustrative example where the jurisdiction of the ultimate parent entity has not enacted the Pillar Two rules

Assume that the group has recorded consolidated revenue (as defined by the OECD) of €750m in at least two of the last four years, which would result in the group being within the scope of the Pillar Two rules. The GloBE effective tax rates in jurisdictions A, B and C are 25%, 22% and 5% respectively.

The status of Pillar Two rules implementation for each of the jurisdictions is as follows:In this scenario, is the consolidated group in jurisdiction A considered to be impacted by the Pillar Two rules for purposes of the disclosure requirements under IAS 12?

AnswerYes. The Pillar Two rules do not apply to the ultimate parent entity, and so no GloBE top-up tax is collected in jurisdiction A. Instead, the jurisdiction of the next intermediate parent entity (jurisdiction B in this example) applies the IIR and imposes top-up tax on the intermediate parent entity for the low-tax jurisdiction C.

Since the group has been impacted by the Pillar Two rules, the disclosure requirements of IAS 12 would be applicable to the consolidated financial statements prepared by the ultimate parent entity.

Applying the Pillar Two rules and determining the impact are likely to be very complex, and this poses a number of practical challenges. Additionally, how to account for the top-up tax (whether GloBE or a GloBE qualifying domestic minimum top-up tax) under IAS 12 was not immediately apparent.

On 23 May 2023, the IASB issued narrow-scope amendments to IAS 12. The amendments provide a temporary exception from the requirement to recognise and disclose deferred taxes arising from enacted or substantively enacted tax law that implements the Pillar Two model rules published by the OECD, including tax law that implements QDMTT described in those rules.

The amendments to IAS 12 make it clear that entities subject to Pillar Two rules must ignore the deferred tax implications of enacted or substantively enacted Pillar Two legislation in their IFRS® financial statements. However, for annual reporting periods beginning on or after 1 January 2023, these entities will need to provide some additional disclosures about current taxes in their annual financial reports, as described below.

As explained above, the one impact is that entities are prohibited from recognising or disclosing deferred tax implications arising from Pillar Two. A second impact is that the narrow-scope amendments to IAS 12 introduced targeted disclosure requirements for affected companies. They require entities to disclose:

Due to the complexity of the Pillar Two rules, we expect that it will take time for some entities to carry out their impact assessments following the legislation’s announcement. As a result, management might be unable to quantify and therefore disclose the detailed effects. However, an entity might be able to provide qualitative information – for example, if a material portion of its business operates in relatively low-tax jurisdictions that are likely to be impacted.

A parent entity might be in a jurisdiction where the Pillar Two legislation is substantively enacted, but not yet in effect at the group’s reporting date. For example, as of 31 December 2023 the jurisdiction of the parent entity might have substantively enacted the Pillar Two legislation that will become effective from 1 January 2025.

To meet the disclosure requirements of IAS 12 above, an entity that is within the scope of the Pillar Two rules should disclose qualitative and quantitative information about its exposure to Pillar Two income taxes in its annual financial statements as of 31 December 2023. That information need not necessarily reflect all of the specific requirements of the legislation and could be provided in the form of an indicative range.

Disclosures that might be considered are as follows:

For example, if the parent has subsidiaries that operate in low-tax jurisdictions, it might consider disclosing the name and the current legislative or average effective tax rates of those jurisdictions.

To the extent that information is not known or reasonably estimable, the entity should instead disclose a statement to that effect and information about its progress in assessing its exposure. Management will need to be able to support any statement that Pillar Two will not have a material impact.

An illustrative example of what an entity might consider disclosing in its financial statements for the year ended 31 December 2023 is as follows.

OECD Pillar Two model rulesThe group is within the scope of the OECD Pillar Two model rules. Pillar Two legislation was enacted in country X, the jurisdiction in which the company is incorporated, and will come into effect from 1 January 2025. Since the Pillar Two legislation was not effective at the reporting date, the group has no related current tax exposure. The group applies the exception to recognising and disclosing information about deferred tax assets and liabilities related to Pillar Two income taxes, as provided in the amendments to IAS 12 issued in May 2023.

Under the legislation, the group is liable to pay a top-up tax for the difference between its GloBE effective tax rate per jurisdiction and the 15% minimum rate. All entities within the group have an effective tax rate that exceeds 15%, except for one subsidiary that operates in jurisdiction A.

For 2023, the average effective tax rate (calculated in accordance with para 86 of IAS 12) of the entity operating in jurisdiction A is:

Group entity operating inThe group is in the process of assessing its exposure to the Pillar Two legislation for when it comes into effect. This assessment indicates for jurisdiction A that the average effective tax rate based on accounting profit is 8.3% for the annual reporting period to 31 December 2023. However, although the average effective tax rate is below 15%, the group might not be exposed to paying Pillar Two income taxes in relation to jurisdiction A. This is due to the impact of specific adjustments envisaged in the Pillar Two legislation which give rise to different effective tax rates compared to those calculated in accordance with paragraph 86 of IAS 12.

Due to the complexities in applying the legislation and calculating GloBE income, the quantitative impact of the enacted or substantively enacted legislation is not yet reasonably estimable. Therefore, even for those entities with an accounting effective tax rate above 15%, there might still be Pillar Two tax implications. The group is currently engaged with tax specialists to assist it with applying the legislation.

Entities might consider disclosing the expected impact of Pillar Two if the local jurisdiction has not yet announced or enacted the changes before the financial statements are authorised for issue. [IAS 1 para 17(c)].

Disclosure example – legislation not substantively enactedIn December 2021, the Organisation for Economic Co-operation and Development (OECD) issued model rules for a new global minimum tax framework (Pillar Two), and various governments around the world have issued, or are in the process of issuing, legislation on this. In [Country X], the government released draft legislation on Pillar Two in [July 2023]. The group is in the process of assessing the full impact of this.

The cash tax impact of the Pillar Two rules on going concern should be reflected in that assessment once the local legislation is announced rather than from when it is substantively enacted. This is because the going concern assessment includes all ‘expected’ future cash outflows and takes into account all available information about the future. [IAS 1 para 26].

Similarly, if an entity applies post-tax cash flows in a value-in-use calculation of the recoverable amount of an asset or a cash-generating unit when performing an impairment test, the cash tax impact of the Pillar Two rules should be reflected in those cash flows. The timing of this would be based on a market participant’s view which would likely be once the local legislation is announced rather than from when it is substantively enacted. Generally, the inclusion of tax cash flows would not impact the recoverable amount, because the entity would also adjust the post-tax discount rate used (see FAQ 24.87.2).

Timeline for impact of Pillar Two on accountingThe disclosure requirements will depend on the extent to which Pillar Two legislation has been enacted in the jurisdictions in which the group operates and whether it is in effect. The timeline below sets out the required disclosures at the various stages of the process.

It also illustrates when the impact of top-up taxes should be considered in the going concern assessment and in impairment tests.

Some reporting entities might need to consider the Pillar Two requirements before the amendments to IAS 12 are effective in their jurisdiction – for example, where a multinational entity within the scope of the Pillar Two model rules has a period end that falls after the date when Pillar Two legislation is enacted (or substantively enacted) in the entity’s jurisdiction, but before the date when the amendments to IAS 12 providing the exception for deferred tax accounting becomes effective or is endorsed (if there is any local endorsement process in the entity’s jurisdiction). Reporting entities that need to consider the Pillar Two requirements before the IAS 12 amendments are endorsed might still be able to avoid recognition of deferred tax that would have arisen from the implementation of Pillar Two rules.

In determining whether deferred tax should be recognised at the reporting date, entities should consider that there is an indication in the Basis for Conclusions of IAS 12 (at para BC99(b)) that the IASB did not conclude whether there would be deferred tax implications if no exception was proposed. In fact, the Basis for Conclusions paragraph highlights that respondents were unclear as to whether and how IAS 12 would be applied, confirming that the existing requirements are unclear.

Affected entities might need to develop an accounting policy in accordance with paragraph 10 of IAS 8, ‘Accounting Policies, Changes in Accounting Estimates and Errors’. In developing that policy, entities might conclude that Pillar Two legislation does not require adjustments or additions to the existing deferred tax balances. In developing an accounting policy, an entity might consider:

Listed entities should take into account any views of their local regulator in developing an accounting policy.

The Pillar Two rules are intended to be implemented as part of a common approach, as agreed by the OECD members, and to be brought into domestic legislation by 2023. However, each jurisdiction will need to determine if and when the rules will be enacted and effective. For example, at the time of issuing this publication, the Pillar Two rules have been enacted in the United Kingdom and are effective for accounting periods beginning on or after 31 December 2023, except for the UTPR which is still in draft and expected to be effective after 31 December 2024 at the earliest. The EU has issued a Directive to require its Member States to enact domestic legislation for the IIR from 2024 and the UTPR from 2025. For the status of Pillar Two implementation in different countries and regions, visit PwC’s Pillar Two Country Tracker.

The amendments to IAS 12 are required to be applied immediately (subject to any local endorsement processes) and retrospectively in accordance with IAS 8, including the requirement to disclose the fact that the exception has been applied if the entity’s income taxes will be affected by enacted or substantively enacted tax law that implements the Pillar Two rules. The disclosures relating to the known or reasonably estimable exposure to Pillar Two income taxes are required for annual reporting periods beginning on or after 1 January 2023, but they are not required to be disclosed in interim financial reports for any interim period ending on or before 31 December 2023.

For more about Pillar Two model rules and their impact on businesses, visit PwC’s Pillar Two Readiness microsite.

For more information, contact Dave Walters or Gary Berchowitz.Question 1: Is Pillar Two top-up tax, an income tax expense within the scope of IAS 12 in the separate financial statements of the entity liable to pay the taxes (the parent)? Is Pillar Two top-up tax expense recognised as a tax expense in the parent or in the entity giving rise to the top-up tax (the low-taxed subsidiary)?

The Pillar Two top-up tax expense is an income tax within the scope of IAS 12 and is recognised as an income tax expense in the separate financial statements of the entity liable to pay the top-up tax expense. If the jurisdiction where a parent of a multinational enterprise sits has enacted IIR Pillar Two rules, the parent is the primary obligor of such top-up taxes. In our view the subsidiary entity that gives rise to the top-up taxes should not recognise an expense. This is because the IFRS accounting framework does not generally allow push down accounting. Absent such a requirement, push down accounting is not a permissible accounting policy. An analogy to the requirements in IFRS 2 for group share-based payment arrangements is not appropriate because the subsidiary does not receive any goods or services as a consequence of the parent paying the top-up tax and the tax is not settled by the parent on the subsidiary’s behalf. There may be alternative possible approaches.

Question 2: Does the IAS 12 para 4A scope exception from recognising and disclosing information about deferred tax assets and liabilities related to Pillar Two taxes apply to a Domestic Minimum Top-up Tax (DMTT) that a country has asserted to be ‘qualifying’ but has not yet been peer reviewed?

Yes, the IAS 12 scope exception can typically be applied. Each country is required to self certify whether their DMTT is ‘qualifying’. The self certification is to be subject to a peer review, however the self certified QDMTT is generally assumed to be qualifying until there is a successful challenge to deem it non-qualifying. The expectation is that any removal of qualifying status by the peer review is prospective not retrospective but this has yet to be confirmed.

A non-qualifying DMTT does not apply the exception.Question 3: Paragraph 88C of IAS 12 refers to disclosure of ‘the entity’s exposure to Pillar Two income taxes arising from that legislation’. Does an entity need to disclose all of its exposures relating to Pillar Two legislation including the exposures that do not impact the Pillar Two tax expense?

No. As stated in para BC107 of the basis for conclusions to IAS 12, the para 88C disclosure requirement was brought into the standard as enacted Pillar Two legislation could create exposures that are not yet reflected in an entity’s income tax expense for the period and so there was an information need. The entity’s exposure to be disclosed relates only to the exposures impacting the entity’s income tax expense. It does not relate to exposures impacting other income statement line items, such as adjustments to the measurement of assets because of reduced cash inflows. For example, an investment entity that recognises its investments on a fair value basis might not have a Pillar Two tax expense of its own to account for but its investees might be exposed, ultimately impacting the investees’ fair value. There is no requirement to disclose this exposure under paragraph 88C of IAS 12 although, if the impact on the investees’ fair value going forward could be material, the investment entity might choose to disclose that fact.

Question 4: Should an entity accrue Pillar Two current income taxes in interim financial statements?Yes. IAS 12 para 4A confirms that Pillar Two taxes arising from tax law enacted or substantively enacted to implement the Pillar Two model rules, are income taxes in the scope of IAS 12. IAS 34 para B13 says the same accounting and recognition measurement principles are applied in an interim financial report as are applied in annual financial statements. Therefore, Pillar Two income taxes should be accounted for in interim periods.

Question 5: How should an entity account for Pillar Two income taxes in interim periods?IAS 34 para B12 requires the interim period income tax expense to be accrued using the tax rate that is applicable to expected total annual earnings, that is, the estimated average annual effective income tax rate is applied to the pre-tax income of the interim period. Taxation is assessed based on annual results and, accordingly, determining the tax charge for an interim period will involve making an estimate of the likely effective tax rate for the year.

IAS 34 para B14 requires, to the extent practical, a separate estimated average annual effective income tax rate to be determined for each taxing jurisdiction and for that rate to be applied individually to the interim period pre-tax income of each jurisdiction.

To apply these requirements an entity will need to estimate its annual effective tax rate for each jurisdiction including P2. The calculation of the effective tax rate should be based on an estimate of each jurisdiction’s income tax charge for the year (which includes P2) expressed as a percentage of the jurisdiction’s expected accounting profit. This percentage is then applied to the jurisdiction’s interim result, and the tax is recognised ratably over the year as a whole.